Contrary to popular belief, inflation did not lead to the downfall of incumbents worldwide.

The Presidential election was a disaster for Democrats. There’s been no shortage of think pieces, posts, and punditry seeking to explain why Harris was trounced while down ballot candidates significantly outran the top of the ticket. Aside from the usual blame game, in this case centrists mostly accusing the Left of being too accepting of trans people, another explanation quickly became adopted as a given: Harris was virtually destined to lose as voters across the globe punished incumbents for COVID related inflation.

This theory has spread its tentacles across the ideological spectrum. Spearheaded initially by Matt Yglesias both pre (2023) and post election, it has since gained steam—though with varying boundaries, implications, and suggested remedies—namely via Derek Thompson in The Atlantic, Noah Berlatsky in Public Notice, John Burn-Murdoch in the Financial Times, and David Dayen at The American Prospect.

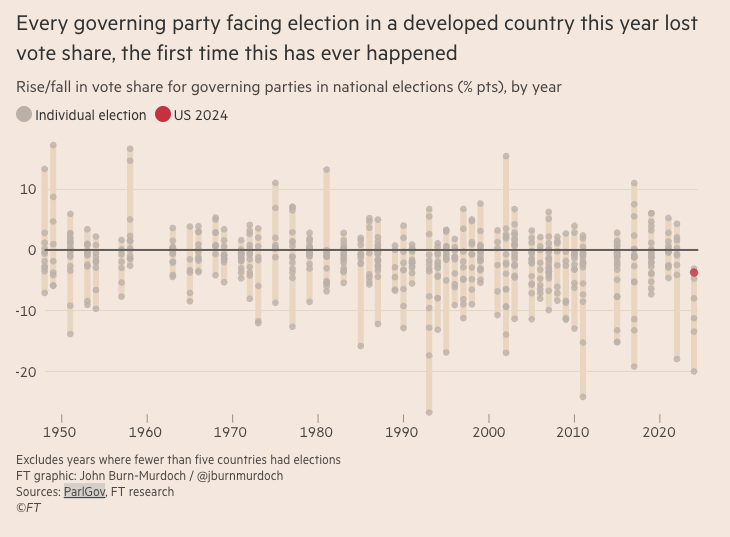

On the surface, it’s rather convincing. Burn-Murdoch’s piece included a chart, which has been widely circulated, displaying research from ParlGov stating that all incumbent parties in developed countries (though the text of his piece says “major countries”) have lost vote share in 2024 national elections, a previously unseen phenomenon.

That’s pretty damning. But wait, what’s a major country? And why is 2024 the relevant data set while 2023 is omitted? If an incumbent party had a slightly lower vote share but remained in power, doesn’t that indicate something other than voters wanting to kick out the incumbents?

In other words, is the theory of inevitability that holds that Harris was destined to lose, rather than win, narrowly due to inflation really true in any meaningful sense? To the extent it bears out, does it even provide useful lessons? When incumbents lose seats in a parliamentary system, is that always the same as the American two-party elections? We would argue no. The reality is much more complex, as this piece lays out. Arbitrary decisions with respect to what elections count, whether 2023 elections were as inevitable, and whether it matters that Democrats were not wholly the incumbent party (the House of Representatives exists, even if none of the people who articulate this theory really acknowledge it).

To start with, Burn-Murdoch’s chart does not include Mexico in its 2024 data set, either because he doesn’t see Mexico as a major or developed country—rather offensive, a $1.79 trillion GDP says otherwise—or because it runs contrary to the other examples. In June, Mexico’s incumbent party won a landslide reelection victory, with now-President Claudia Sheinbaum winning 59.4% of the vote, improving significantly upon her predecessor’s 53.2% in 2018. To their credit, Dayen and Yglesias (in one of his several pieces touching on the matter) do acknowledge Mexico as an exception to the rule, but say that high-inflation prior to COVID likely accounts for why the incumbents were not punished. It’s true that Mexico is historically prone to bouts of inflation, but their inflation rate had fallen to 3.64% in 2019 and 3.4% in 2020 before spiking to 5.69% in 2021 and 7.9% in 2022. Even if Mexican voters take some inflation as a given, this is still a substantial increase that one would expect to see reflected in the next election according to the supposed globally intertwined and inevitable relationship between incumbent vote share and inflation. It just doesn’t seem correct to say that inflation is so priced-in to Mexican politics that a four percent increase that more than doubles the rate doesn’t phase the population. Indeed, Mexico’s 2018 election came after a spike of inflation, jumping from 2.8% in 2016 to 6% in 2017, and in that case the incumbents were soundly defeated.

While we’re far from experts on Mexican politics, it certainly seems as if the fact that Mexican President Andrés Manuel López Obrador was an entertaining populist who inveighed against the rich helped him—and might have been a useful example for Democrats. Yes, Harris was a potential bundle of firsts—but any more so than a Jewish woman in Mexico? Sheinbaum’s landslide win seems improbable enough to merit more curiosity than it has received from Democratic strategists.

Mexico is the most glaring counterexample, given the dramatic improvement from the prior election and its deep cultural connections to the United States, but it’s not the only place where incumbent parties retained power in 2024. Taiwan’s ruling DPP won the presidential election but came in second place of the legislature by one seat, although they had the higher raw vote total and improved their vote share from 34% in 2020 to 36% in 2024. Taiwan is a highly developed economy, so its results seem highly applicable to the United States. The Dominican Republic’s PRM party won reelection and increased its vote share from 52.5% in 2020 to 57.4% in 2024 after inflation peaked at 8.8%; not a wealthy country, but a fellow North American state that is culturally intertwined with the United States.

Bulgaria, an upper middle income country per the World Bank, held elections in June and October, with the GERB-SDS coalition retaining its plurality in both elections and increasing its vote share by 1.7% in October. (There were allegations of voting irregularities, but these appear to have been vote buying efforts by the fourth place party rather than the winners.) In high income Croatia, the HDZ won a plurality and remains the governing party with 34.4%, a 3% decrease from 2020 but not a bad showing in the face of a peak inflation rate of 10.67%.

Perhaps these examples don’t fit into the arbitrary limits of countries discussed in this theory. And we’re aware that they’re not the most commonly cited counterparts to the United States (although Mexico really ought to be).

But that points to a bigger issue—proponents of the theory have differing parameters of who qualifies. Burn-Murdoch limits it to 2024 and “major countries.” Yglesias in his New York Times op-ed says there are no examples of incumbents in a “rich country securing a strong re-election.” He includes 2023 elections and, in prior pieces, said incumbent losses were occurring in the English-speaking world and called it a dominant global trend. Dayen said “virtually every party that was the incumbent at the time that inflation started to heat up around the world.” Berlasky, citing Yglesias, says it’s “a brutal time for all incumbent parties across the world,” but only touches on Japan, Austria, the UK, and France. Thompson says it’s a “nightmare for incumbent parties around the world” with parties in “major countries” suffering defeats. We’re not saying each iteration of this take is wrong, but the variance of which countries and years are included suggests there is not a consensus on how and why inflation played a role in recent elections, which is the crux of the theory’s relevance.

Limiting such a phenomenon to a vague, undefined category of “major countries” is unhelpful, but it’s understandable why much of the discussion is centered on the 2024 elections. They are more recent and therefore feel more related to Harris’s performance. But, given that COVID-induced inflation rose through 2021 and peaked in 2022, one would expect that elections in 2023 would be particularly disastrous for incumbents while inflation was fresh on minds and felt in pocketbooks. 2024 elections could still be impacted, but surely 2023 would see voters forefronting inflation at least as much as in 2024. So what happened in 2023?

Well, in Greece, the ruling ND party won elections in May and June of 2023, brushing off the 9.3% inflation rate by garnering a greater vote share compared to 2019. In Spain, the ruling PSOE failed to win the most seats, but they increased their vote share by 3.7%, gained two seats, and successfully formed another coalition government. In Estonia, the Reform Party won reelection with a two percent increase in vote share from 2019 when it won the most votes, eventually resulting in a Reform Party-led coalition government in 2021. In Turkey, President Erdogan won reelection with 52% of the vote, down just half a percentage point from 2018. In Luxembourg, the three party coalition government made up of the LSAP, DP and the Green party dissolved after the Greens vote share diminished. However, LSAP and DP were the larger coalition parties, and they increased their vote shares from 2018 with DP joining the top performing CSV party to form a new coalition. These are not all resounding victories, but they are largely continuations of incumbent governments.

There were also, of course, some incumbent losses in the Netherlands, Finland, and Slovakia, but it is a mixed bag rather than a global backlash. I mean, incumbent parties in democracies should sometimes lose—it would be suspicious if they did not! Furthermore, Spain, Estonia, and Luxembourg illustrate the difficulty in drawing black and white conclusions about parliamentary elections. Governing coalitions were altered, but the top parties improved their vote share in a way that does not at all suggest a punishment for presiding over a period of inflation. In other words, it’s complicated.

So what does this tell us about the election here in the US? For one, it tells us that inflation was not the be-all and end-all of what happened in our presidential election. Political parties and their campaigns have agency. They can craft narratives and deliver compelling messages that convince voters to show up for them on election day. Contrary to the now-conventional wisdom, many incumbent parties successfully did so, regardless of inflation.

Center-left proponents of inflations’ preeminence use the theory to claim that COVID-era stimulus spending from Biden and Harris was too strong and the administration was too slow to pivot towards budget hawkery. Inflation was still on the minds of voters, but Harris and Trump were neck and neck on the question of who voters trust on the economy. We also saw down ballot Democrats, who were still incumbents, outperform Harris in a way that puts the inflation-induced predetermination into further question.

There is also a key difference between American elections and parliamentary elections in other countries—Biden-Harris was not in nearly as powerful a position as most ruling parties because he faced an obstructionist House majority. In 1948 Harry Truman ran as the successor to an old president for whom he had served as VP. Truman’s approach could and should have been instructive. Biden and Harris should have presented a series of responses to inflation, fought for them despite the uphill chances in the House, and then run against radical (comically so!) Speaker Johnson and his weirdo corporate lackey caucus. For instance, one of us wrote a piece in July urging the Administration to establish “an Anti-Price-Fixing Division within the DOJ, equipped with substantial new appropriations to enable the government to hire world-class experts and attorneys who can effectively uncover and prosecute corporate criminality.”

If Speaker Johnson’s caucus passed the bill, it would be a tangible accomplishment on a germane issue, and offered Biden and Harris an opportunity to promise a better future on prices. And, more likely, when it failed, Biden and then Harris could blame Johnson for ongoing high prices. Such a political gambit is not available to parties leading parliamentary systems, yet another reason why claiming that Democrats lack the ability to overcome inflation based on election results in some parliamentary systems in 2024 but not 2023 is misguided.

Despite all the fuss about polling errors and fingers-on-scales, polls of the presidential election were more accurate than in previous years, though Trump still outperformed polls by roughly 2 points nationally. Polls were more or less tied in the final days, suggesting that Harris could have done better by sticking with the campaign identity that resulted in a big polling lead after the debate. While inflation and the economy were relevant throughout the campaign, Harris was still, at times, able to spin a narrative and draw a contrast with Trump that brought voters to her side. Of course, Trump declined a second debate, but the campaign did not make him pay a political price for playing chicken. Instead, Harris’ campaign focused the final months on courting Republicans through appearances with Liz Cheney while failing to get endorsements from actually high profile Republicans like George Bush or Mitt Romney. We wouldn’t have loved any Republican first strategy, but if you’re considering that route, you have to know that a handful of former members of the House and Dick Cheney is really not enough.

Democrats knew, or at least should have known, that this would be an uphill battle given the administration’s unpopularity and the late candidate switch. But the campaign did not pursue a bold, antagonistic, shoot-for-the-stars approach that you would expect from a party with their backs against the wall and a purported global trend in Trump’s corner. None of this is to say that inflation didn’t play any role—of course it did. But pundits, and more importantly the party, should not spread the incorrect assessment that all incumbents everywhere were doomed because of it. It only serves as an excuse for the people responsible for the campaign’s failure to shrug their shoulders and say, “oh well, nothing we could have done.” That is nonsense.

IMAGE CREDIT: Vice President Kamala Harris delivers remarks at the kickoff for the Reproductive Freedoms Tour, Monday, January 22, 2024, at the International Union of Painters and Allied Trades (IUPAT) District Council 7 in Big Bend, Wisconsin. (Official White House Photo by Lawrence Jackson)